A few years ago, a public school teacher and a city government employee sat together during a financial planning seminar. Both were earning steady incomes and thinking about retirement, yet they were offered different savings plans: one had a 403(b), while the other had a 457 plan.

Confusion filled the room as they tried to understand the difference between 403(b) and 457, wondering which one offered better benefits, flexibility, and long-term security.

The difference between 403(b) and 457 plans often puzzles beginners and even experienced professionals. While both are tax-advantaged retirement accounts, their rules, withdrawal options, and eligibility vary in meaningful ways.

Understanding the difference between 403(b) and 457 can help individuals make smarter financial decisions and avoid costly mistakes. In fact, knowing the difference between 403(b) and 457 is essential for anyone working in public service or nonprofit sectors.

Key Difference Between the Both

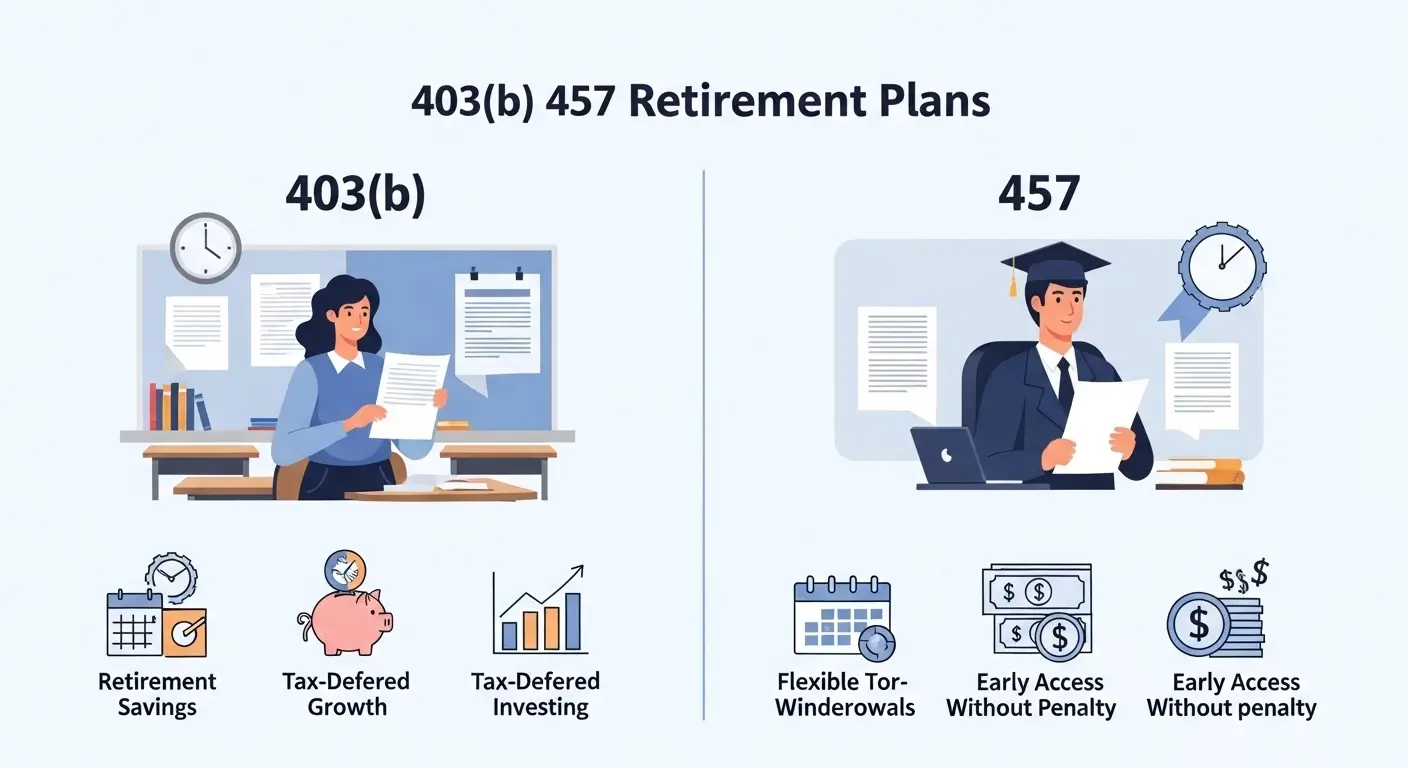

The primary distinction lies in withdrawal flexibility and penalties. A 457 plan allows penalty-free withdrawals before age 59½ after leaving employment, while a 403(b) typically imposes early withdrawal penalties.

Difference Between Dehumidifier and Humidifier :in (2026)

Why Is Their Difference Necessary to Know for Learners and Experts?

Understanding the difference between 403(b) and 457 is important because it directly impacts retirement planning strategies. For learners, it builds foundational financial literacy and helps them choose wisely early in their careers. For experts, it allows precise advising and optimization of tax benefits.

In society, this knowledge empowers individuals especially teachers, healthcare workers, and government employees to secure financial stability. Misunderstanding these plans can lead to unnecessary taxes or missed opportunities for savings, which ultimately affects long-term economic well-being.

Pronunciation of Both Terms

- 403(b)

- US: “four-oh-three bee”

- UK: “four-oh-three bee”

- 457 Plan

- US: “four-five-seven plan”

- UK: “four-five-seven plan”

- Difference Between Restroom and Bathroom: in (2026)

Linking Hook

Now that you understand the basic idea, let’s explore the difference between 403(b) and 457 in depth to uncover what truly sets them apart.

H2: Difference Between 403(b) and 457

1. Eligibility

- 403(b): Offered to employees of public schools and nonprofits.

- Example 1: A teacher contributes to a 403(b).

- Example 2: A nurse at a nonprofit hospital uses a 403(b).

- 457: Designed for state and local government employees.

- Example 1: A city clerk uses a 457 plan.

- Example 2: A police officer contributes to a 457.

2. Early Withdrawal Rules

- 403(b): Penalty applies before age 59½.

- Example 1: Early withdrawal leads to a 10% penalty.

- Example 2: A teacher pays extra tax when withdrawing early.

- 457: No early withdrawal penalty after leaving the job.

- Example 1: A retired officer withdraws freely at 50.

- Example 2: A city employee accesses funds without penalty.

3. Contribution Limits

- 403(b): Standard IRS limits apply.

- Example 1: Annual capped contributions.

- Example 2: Employer matching may apply.

- 457: Similar limits but includes special catch-up options.

- Example 1: Extra contributions before retirement.

- Example 2: Double contribution in final years.

4. Employer Type

- 403(b): Nonprofits and educational institutions.

- Example 1: Charity organizations.

- Example 2: Universities.

- 457: Government entities.

- Example 1: Municipal offices.

- Example 2: State departments.

5. Investment Options

- 403(b): Often limited (annuities, mutual funds).

- Example 1: Fixed annuity plans.

- Example 2: Basic mutual funds.

- 457: Broader investment choices.

- Example 1: Stocks and bonds.

- Example 2: Diverse portfolios.

6. Rollover Options

- 403(b): Can roll into IRA or 401(k).

- Example 1: Teacher switches jobs and rolls over funds.

- Example 2: Funds moved to IRA.

- 457: Rollover options exist but may be limited.

- Example 1: Government employee transfers funds.

- Example 2: Restrictions apply in some cases.

7. Catch-Up Contributions

- 403(b): Age-based catch-up.

- Example 1: Extra contributions after 50.

- Example 2: Long-term employees get additional benefits.

- 457: Special catch-up provisions.

- Example 1: Double limit before retirement.

- Example 2: Unique government plan advantages.

8. Risk and Security

- 403(b): Depends on provider (sometimes insurance-based).

- Example 1: Annuity risk.

- Example 2: Insurance-backed plans.

- 457: Government-backed, generally stable.

- Example 1: Public sector reliability.

- Example 2: Lower default risk.

9. Loan Availability

- 403(b): Loans are often allowed.

- Example 1: Borrow against savings.

- Example 2: Repay through payroll.

- 457: Loans less common.

- Example 1: Limited borrowing options.

- Example 2: Strict rules apply.

10. Tax Treatment

- 403(b): Tax-deferred contributions.

- Example 1: Lower taxable income now.

- Example 2: Pay taxes at retirement.

- 457: Also tax-deferred but more flexible withdrawals.

- Example 1: Deferred taxation.

- Example 2: Easier access later.

Nature and Behaviour of Both

A 403(b) behaves like a traditional retirement savings plan focused on long-term growth with stricter withdrawal rules. It encourages disciplined saving.

A 457 plan, on the other hand, is more flexible and adaptable, allowing earlier access to funds and catering to government employees who may retire earlier.

Why People Are Confused About Their Use

People confuse them because both offer tax advantages, have similar contribution limits, and serve retirement purposes. The names (numbers) also make them seem technical and nearly identical, masking their practical differences.

Table: Difference and Similarity Between 403(b) and 457

| Feature | 403(b) | 457 | Similarity |

| Eligibility | Nonprofits | Government | Both for specific sectors |

| Withdrawal | Penalty before 59½ | No penalty after leaving job | Retirement-focused |

| Tax Benefit | Tax-deferred | Tax-deferred | Reduce taxable income |

| Investment | Limited | Broader | Growth-oriented |

| Contribution | IRS limit | Similar limit | Savings plans |

Which Is Better in What Situation?

A 403(b) is better for individuals working in nonprofit organizations or education who want structured retirement savings with employer matching. It suits those who prefer disciplined, long-term investment strategies and do not need early access to funds.

A 457 plan is better for government employees who may retire earlier or need flexibility. It allows penalty-free withdrawals after leaving the job, making it ideal for those planning early retirement or career transitions.

Metaphors and Similes

- 403(b): Like a “locked treasure chest” that opens at the right time.

- 457: Like a “flexible savings wallet” you can access when needed.

Connotative Meaning

- 403(b): Positive (discipline, stability), Neutral in technical use

- Example: “Her 403(b) ensured a secure future.”

- 457: Positive (flexibility, freedom), Neutral in context

- Example: “The 457 plan gave him early retirement freedom.”

Idioms or Proverbs

(No direct idioms exist, but applicable ones include:)

- “Save for a rainy day.”

- Example: Both 403(b) and 457 help you save for a rainy day.

- “Don’t put all your eggs in one basket.”

- Example: Use both plans to diversify savings.

Works in Literature (Conceptual References)

- The Intelligent Investor – Benjamin Graham (Finance, 1949)

- Rich Dad Poor Dad – Robert Kiyosaki (Finance, 1997)

- Your Money or Your Life – Vicki Robin (Personal Finance, 1992)

Movies Related to Financial Planning Themes

- The Pursuit of Happyness (2006, USA)

- Wall Street (1987, USA)

- The Big Short (2015, USA)

Frequently Asked Questions

1. What is the main difference between 403(b) and 457?

The main difference is withdrawal flexibility 457 plans allow penalty-free early withdrawals after leaving a job.

2. Can I have both plans?

Yes, if eligible, you can contribute to both simultaneously.

3. Which plan is safer?

Both are safe, but 457 plans are often backed by government entities.

4. Are contributions tax-free?

They are tax-deferred, not tax-free.

5. Which is better for early retirement?

A 457 plan is generally better due to flexible withdrawal rules.

How Both Are Useful for Surroundings

Both plans contribute to financial stability in society. They help individuals prepare for retirement, reduce dependence on public support systems, and promote economic security within communities.

Final Words for Both

The difference between 403(b) and 457 lies not just in rules but in how they serve different professional groups. Each plan has its strengths, and understanding them allows individuals to maximize benefits effectively.

Conclusion

In summary, understanding the difference between 403(b) and 457 is crucial for making informed retirement decisions. While both plans offer tax advantages and long-term savings opportunities, their differences in withdrawal rules, eligibility, and flexibility set them apart.

A 403(b) suits those seeking structured, disciplined savings, whereas a 457 plan offers greater accessibility and freedom. By recognizing these distinctions, individuals can align their financial strategies with their career paths and retirement goals. Ultimately, the right choice depends on personal circumstances, employment type, and future plans.

Henry is a passionate English professor, language specialist, and the founder of SpellCompare.com. With years of academic experience and a deep understanding of grammar, vocabulary, and linguistic nuances, he has dedicated his career to helping students and writers master the English language with clarity and confidence.

As an expert in word comparisons, spelling differences, and grammar rules, Henry simplifies complex language concepts into easy-to-understand explanations. His mission is to eliminate confusion between commonly misused words and provide accurate, research-based guidance that improves writing skills for learners worldwide.

Through SpellCompare.com, Henry combines academic expertise with practical examples, creating content that is clear, reliable, and reader-friendly. His work focuses on precision, correctness, and helping others communicate effectively in both academic and professional settings.

When he’s not teaching or writing, Henry continues researching evolving language trends to ensure his content remains current, helpful, and authoritative.