A few years ago, a public school teacher and her friend working in a private company sat down to plan their retirement. Both were saving diligently, yet they realized they were using completely different systems, one contributing to a 457 plan and the other to a 401(k). This sparked confusion and curiosity about the difference between 401(k) and 457 plans.

Understanding the difference between 401(k) and 457 is crucial because these retirement savings plans may look similar but operate quite differently. If you’re a government employee or working in the private sector, knowing the difference between 401(k) and 457 helps you make smarter financial decisions. Many people search for the difference between 401(k) and 457 to avoid costly mistakes in retirement planning and maximize their benefits over time.

Pronunciation of Both Terms

- 401(k)

- US: four-oh-one-kay /ˌfɔːr.oʊ.wʌn ˈkeɪ/

- UK: four-oh-one-kay /ˌfɔːr.əʊ.wʌn ˈkeɪ/

- 457 Plan

- US: four-five-seven /ˌfɔːr.faɪvˈsɛv.ən/

- UK: four-five-seven /ˌfɔː.faɪvˈsɛv.ən/

- Difference Between VOO and VTI: in (2026)

A Quick Hook Before We Dive Deeper

At first glance, both plans seem like simple retirement tools but once you explore the details, the difference between 401(k) and 457 becomes a game-changer for your financial future.

Difference Between the Keywords

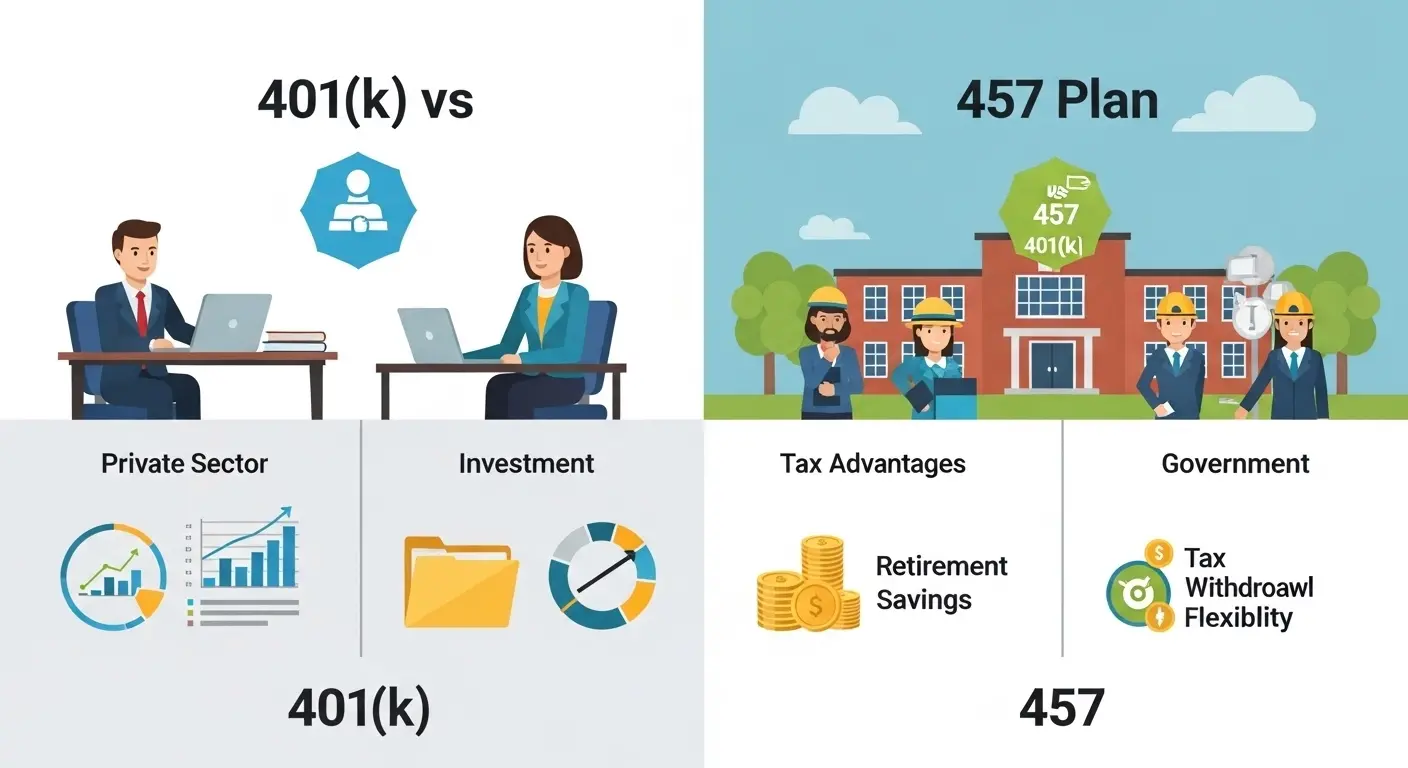

1. Employer Type

- 401(k): Offered by private companies

- Example 1: A tech company offers a 401(k) to its employees

- Example 2: A retail chain provides 401(k) benefits

- 457: Offered by government or non-profit organizations

- Example 1: A state government offers a 457 plan

- Example 2: A public school system provides a 457 plan

- Difference Between LP and EP: in (2026)

2. Early Withdrawal Penalty

- 401(k): 10% penalty before age 59½

- Example 1: Withdraw at 50 → penalty applies

- Example 2: Emergency withdrawal → still penalized

- 457: No early withdrawal penalty

- Example 1: Retire at 55 → no penalty

- Example 2: Leave job early → still penalty-free

3. Contribution Limits

- 401(k): Standard IRS limit applies

- Example 1: Annual cap fixed by IRS

- Example 2: Catch-up contributions after 50

- 457: Similar limits but special catch-up options

- Example 1: Double contributions near retirement

- Example 2: Unique government allowances

4. Availability

- 401(k): Widely available

- Example 1: Corporate jobs

- Example 2: Private startups

- 457: Limited to public sector

- Example 1: Government jobs

- Example 2: Non-profit organizations

5. Withdrawal Flexibility

- 401(k): Strict rules

- Example 1: Hardship withdrawal required

- Example 2: Loan restrictions

- 457: More flexible

- Example 1: Access after leaving job

- Example 2: No age restriction penalties

6. Employer Matching

- 401(k): Often includes matching

- Example 1: Company matches 5%

- Example 2: Bonus contributions

- 457: Rarely includes matching

- Example 1: Government rarely matches

- Example 2: Non-profits may not offer matching

7. Plan Types

- 401(k): Traditional and Roth

- Example 1: Pre-tax contributions

- Example 2: Roth after-tax option

- 457: Also offers similar options

- Example 1: Traditional 457

- Example 2: Roth 457

8. Risk Level

- 401(k): Market-dependent

- Example 1: Stocks fluctuate

- Example 2: Mutual funds risk

- 457: Similar investment risk

- Example 1: Bonds or stocks

- Example 2: Managed portfolios

9. Double Contribution Option

- 401(k): Limited to one plan

- Example 1: Only one employer plan

- Example 2: Cannot double easily

- 457: Can contribute alongside 401(k)

- Example 1: Dual savings strategy

- Example 2: Higher retirement savings

10. Purpose

- 401(k): General retirement savings

- Example 1: Corporate employees

- Example 2: Long-term wealth

- 457: Tailored for public workers

- Example 1: Teachers

- Example 2: Government officers

Nature and Behavior of Both

- 401(k): Structured, strict, and widely adopted. It focuses on long-term disciplined savings with penalties to discourage early withdrawals.

- 457: Flexible and forgiving. It allows easier access to funds, making it suitable for people with uncertain retirement timelines.

Why People Are Confused About Their Use

People confuse them because both are tax-advantaged retirement plans with similar contribution limits and investment options. The names (401(k) and 457) are also numerical and not self-explanatory, making them harder to distinguish.

Table: Difference and Similarity

| Feature | 401(k) | 457 | Similarity |

| Employer | Private | Government | Both employer-sponsored |

| Penalty | Yes | No | Retirement focus |

| Contribution | Limited | Flexible catch-up | Tax advantages |

| Matching | Common | Rare | Long-term savings |

| Access | Restricted | Flexible | Investment growth |

Which is Better in What Situation?

A 401(k) is better for private-sector employees who benefit from employer matching. It helps build disciplined savings over time and offers strong long-term growth potential.

A 457 plan is better for government employees or those who may need early access to funds. Its flexibility makes it ideal for early retirees or people planning career changes.

Metaphors and Similes

- 401(k): Like a locked treasure chest secure but not easy to open early

- 457: Like a flexible wallet accessible when needed

Connotative Meaning

- 401(k): Positive (security), Neutral (restriction), Negative (limited flexibility)

- Example: “His 401(k) gave him peace of mind.”

- 457: Positive (freedom), Neutral (less common), Negative (less employer support)

- Example: “Her 457 plan gave her financial flexibility.”

Idioms or Proverbs

While no direct idioms exist:

- “Don’t put all your eggs in one basket” → applies to both plans

- Example: Invest in both 401(k) and 457 for diversification

Works in Literature

- No major literary works directly titled:

- 401(k) (Finance guides, 2000s, Non-fiction)

- 457 Plan (Retirement planning books, 2010s, Non-fiction)

Movies Related to the Keywords

- Not directly based on these plans, but finance-themed:

- The Big Short (2015, USA)

- Wall Street (1987, USA)

FAQs

1. Can I have both a 401(k) and a 457?

Yes, if eligible, you can contribute to both.

2. Which plan has no early withdrawal penalty?

The 457 plan.

3. Is a 401(k) better than a 457?

It depends on your job and financial goals.

4. Who qualifies for a 457 plan?

Government and some non-profit employees.

5. Do both plans offer tax benefits?

Yes, both provide tax advantages.

How Both Are Useful for Surroundings

Both plans promote financial stability in society. They reduce dependency on public welfare systems and encourage individuals to plan responsibly for retirement.

Final Words for Both

- 401(k): Reliable, structured, and widely trusted

- 457: Flexible, accessible, and strategic

Conclusion

Understanding the difference between 401(k) and 457 is essential for making informed financial decisions. While both plans aim to secure your future, their rules, flexibility, and accessibility vary significantly. A 401(k) suits those seeking structured growth with employer support, while a 457 plan offers flexibility for early access.

By knowing their differences, you can align your retirement strategy with your lifestyle and career path. Ultimately, the right choice depends on your employment type, financial goals, and risk tolerance.

SwiftHarbor is a dedicated English professor, language researcher, and the founder of SpellCompare.com. With years of academic experience in English grammar, vocabulary development, and linguistic comparison, SwiftHarbor specializes in simplifying complex language rules into clear, practical explanations.

As an expert in word usage, spelling differences, and commonly confused terms, SwiftHarbor has helped thousands of learners improve their writing accuracy and communication skills. Through SpellCompare.com, he provides detailed comparisons, easy examples, and research-based insights that make English learning accessible for students, writers, and professionals worldwide.

Known for a clear teaching style and structured explanations, SwiftHarbor focuses on eliminating confusion between similar words, improving grammar confidence, and promoting precise communication. His mission is simple: to make English easier, clearer, and more powerful for everyone.